A communication with important information about how churches report their pastors’ (and lay employees’) income with regard to health insurance premiums is being sent to each Church of the Brethren congregation. The joint letter is from Mary Jo Flory-Steury, associate general secretary of the Church of the Brethren and executive of the Ministry Office, and Scott W. Douglas, BBT director of Employee Benefits. An additional letter from Douglas gives information about IRS rules for Section 105 HRA pre-tax insurance contributions.

Pastors and church workers who have their premium paid at least in part by the church but who are not in a bona fide church group health plan no longer can claim a pre-tax benefit on those payments, explained BBT president Nevin Dulabaum. “The IRS quietly changed the ruling for 2014 and we don’t believe that many pastors are aware of it,” Dulabaum said. “We fear that they’re going to prepare their taxes in April and find that they have several thousand dollars tax liability.”

To tax or not to tax

The joint communication from the Ministry Office and BBT began with the question, “To tax or not to tax–how should premiums for a pastor’s individual medical insurance be handled?”

“If your church is purchasing medical insurance for any of its employees, please read this letter carefully,” the communication said, in part. “Starting in 2014 the new healthcare legislation known as the Affordable Care Act (ACA), now requires employers, in certain situations, to report the cost of providing medical insurance for employees as regular income to those employees.

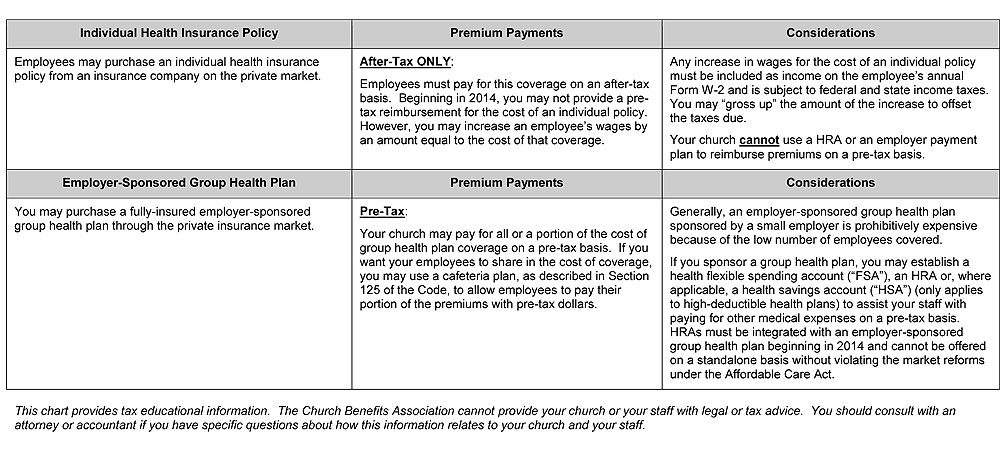

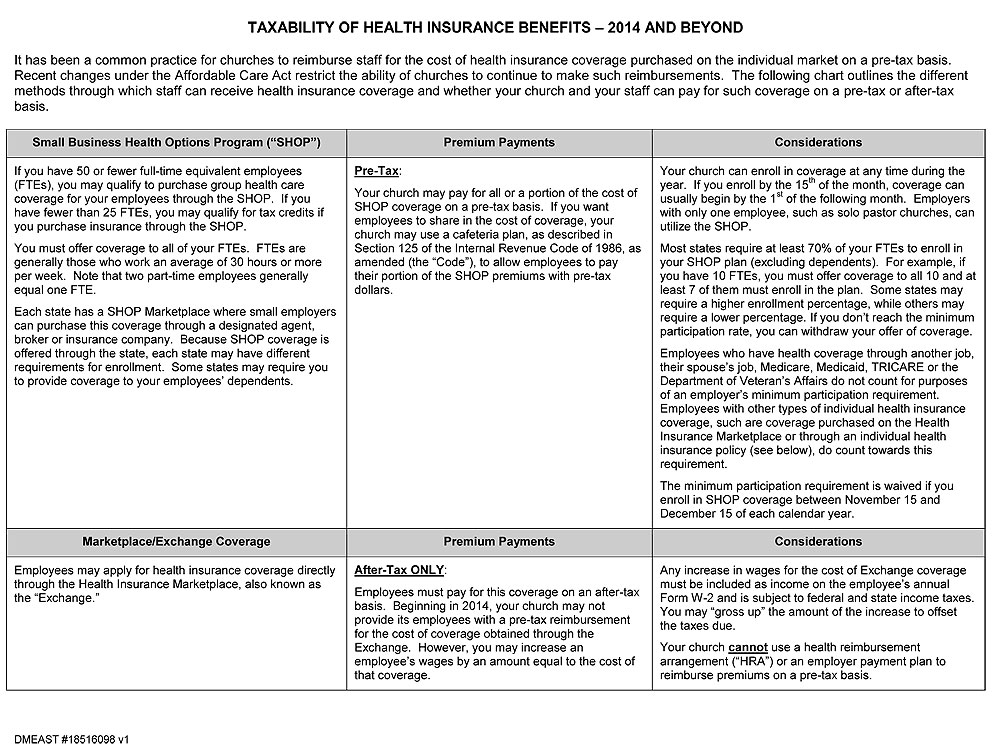

“Who is impacted by this change? Those employers who purchase an individual medical insurance policy directly for their employee(s) or reimburse their employee(s) for the cost of an individual medical insurance policy must now report the money spent for this coverage as regular income paid to the employee(s). Please note: If your church provides medical insurance through a group plan, there is no change to the way that expense is treated for tax purposes.”

HRA not a solution for pre-tax insurance premium purchase

“We have received several inquiries regarding the possibility of purchasing individual health insurance policies through a Section 105 HRA, creating a pre-tax status for this income,” Douglas added in his letter. “Please be aware that unless an employer provides group medical insurance, the money used to purchase individual medical insurance must be reported as earned (taxable) income to the employee.”

An HRA is not a solution for avoiding the tax consequences of the Affordable Care Act market reforms, and using this method could result in heavy fines, the letter warns.

Douglas noted that legal counsel has offered this information in regard to the subject of pre-tax insurance contributions:

On May 13, 2014, the IRS issued a Question and Answer “Q&A” document reiterating that employers are prohibited from reimbursing employees on a pre-tax basis for premiums employees pay for individual health insurance policies, either in or outside the Exchange/Marketplace. The Q&A cited IRS Notice 2013-54 and PPACA market reforms. The IRS Q&A does not prohibit employers from increasing employees’ compensation so they can purchase individual health insurance policies. For more information go to www.irs.gov/uac/Newsroom/Employer-Health-Care-Arrangements .

IRS Notice 2013-54 states the following, clearly indicating that an HRA may not be used to purchase medical insurance for employees from the individual insurance market on a “pre-tax” basis: “…(a) for purposes of the annual dollar limit prohibition, an employer-sponsored HRA cannot be integrated with individual market coverage or with individual policies provided under an employer payment plan, and, therefore, an HRA used to purchase coverage on the individual market under these arrangements will fail to comply with the annual dollar limit prohibition….”

“While BBT does not advise clients, we strongly discourage you from using an HRA arrangement to purchase medical insurance for purposes of pre-tax benefits,” Douglas wrote.

|