On Dec. 22, 2017, the Tax Cuts and Jobs Act of 2017 (TCJA) was passed by Congress and signed into law by the President. This far-reaching legislation contained the largest changes to the tax code since the Tax Reform Act of 1986. Most of the changes, however, “sunset” after 2025, which means they are currently understood to be temporary.

The forms

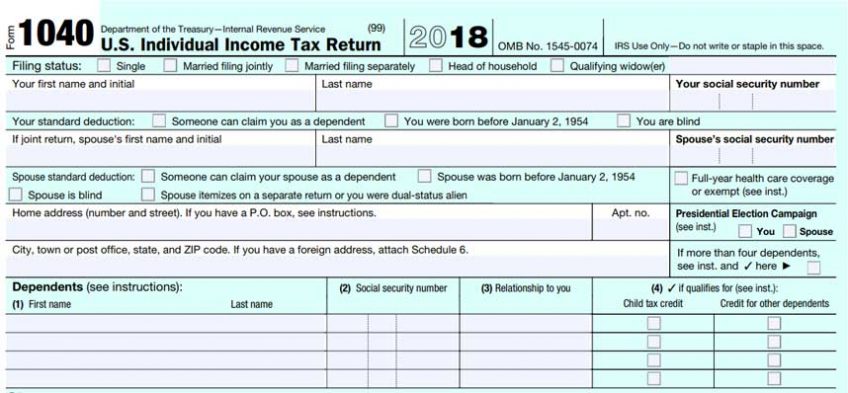

Gone are all the forms we know and love: the 1040EZ, the 1040A, and the “long form” 1040. The new 1040 consists of two half-page forms (the “postcard”) and six attached schedules. Basically, the long form 1040 has been separated out from two pages to eight. Since the IRS kept the same line numbers on the expanded schedules, it’s easy to see that this is exactly what they did.

The Form 1040 “postcard” has six attached schedules including Schedule 1: Additional Income and Adjustments to Income, Schedule 2: Tax, Schedule 3: Nonrefundable Credits, Schedule 4: Other Taxes, Schedule 5: Other Payments and Refundable Credits, and Schedule 6: Foreign Address and 3rd Party Designee. Most American taxpayers won’t need this last schedule.

That’s just the changes in the appearance of the forms. The substance has changed quite a bit as well.

Deductions

How do deductions work and what do they do? To put it simply, deductions reduce income dollar-for-dollar, before income tax is calculated. These deductions have been changed extensively.

The most well-known deduction is the personal exemption, which in 2017 reduced taxable income by $4,050 per person listed on the tax return. This deduction has been eliminated completely by the TCJA.

Another well-known deduction is the standard deduction, which has been greatly increased for 2018. This deduction is used by taxpayers who do not use Schedule A to itemize their deductions.

Since the goal of deductions is to reduce taxable income (thus reducing income tax), the larger deduction (whether the standard deduction or itemized deductions) should always be used.

The tuition and fees deduction, an education-related deduction, has not been renewed for 2018.

Changes have been made to the moving expenses deduction. Only members of the US Armed Forces can deduct their moving expenses. For all other employees, employer reimbursements or direct payments for moving are now taxable income to the employee. For pastors, this means both income tax and self-employment taxes must be paid on the cost of a move.

The qualified business income deduction is a new deduction available for sole proprietors, partnerships, s-corporations, trusts, and estates. Very simply put, it permits business owners to deduct up to 20 percent of their qualified business income, in addition to other business expenses. It is a complicated calculation that even professional tax software doesn’t always get right. That’s because it interacts with the rest of the tax return by including limits and phaseouts based on the total taxable income on the return (including the spouse’s income, if applicable). It also imposes further restrictions on claiming the deduction on a set of businesses listed as “specified service trades or businesses.”

The alimony deduction has changed depending on when the divorce was finalized or the divorce decree was modified. Everything remains the same if a divorce was finalized (or a divorce decree was modified) before Jan. 1, 2019. Alimony paid is still deductible, and alimony received is still included in taxable income. However, if a divorce was finalized (or a divorce decree was modified) after Dec. 31, 2018, alimony no longer appears on the tax return. Alimony paid will no longer be deductible, and alimony received will no longer be included in income.

On Schedule A, itemized deductions also have significantly changed. Here is a review of this form, section by section:

- Medical expenses. Medical expenses have a threshold of 7.5 percent of adjusted gross income (AGI) before any expenses can be deducted. For example, if you have an AGI of $10,000 and medical expenses of $1,000, the first 7.5 percent ($750) cannot be deducted. Only the expenses above the threshold can be deducted. This threshold is actually down from 10 percent for 2018 and 2019, after which the threshold will return to 10 percent.

- State and local taxes (SALT). This section, which includes state and local income taxes, sales taxes, real estate taxes, personal property taxes, and other taxes, is now limited to a total of $10,000. Homeowners in high-tax states will feel this limitation.

- Mortgage interest. Deductible mortgage interest is limited to home acquisition debt up to $750,000, lowered from $1,000,000.

- Charitable contributions. Donations can now be claimed up to 60 percent of the donor’s AGI, which is an increase from 50 percent of AGI.

- Casualty and theft losses. These losses have been severely limited. Casualty and theft loss claims can be deducted only if the claims were caused by a Presidentially-declared disaster. Deductions are no longer allowed for individual events like fire or theft.

- Job expenses and certain miscellaneous deductions. This section has been deleted in full. These deductions included unreimbursed employee expenses (including books, supplies, business mileage, business-related education); the cost of tax preparation (software, paying a professional, etc.); safety deposit box rentals; investment management fees and other investment expenses (books, courses, etc.).In an important note, pastors are still able to deduct their unreimbursed business expenses against their self-employment income using IRS Publication 517, Clergy Worksheet 3, line 6.Form 2106, “Employee Business Expenses,” still exists. Before the TCJA, this form was used for unreimbursed expenses subject to a threshold of 2 percent of AGI. Now this form is used for miscellaneous business expenses not subject to the 2 percent AGI threshold. Only certain employees qualify to use this form: Armed Forces reservists, qualified performing artists, fee-basis state or local government officials, and disabled employees with impairment-related work expenses.

Credits

While deductions are terrific, credits are even better! Credits reduce income tax, dollar-for-dollar. Credits come in two types: non-refundable and refundable. Non-refundable credits reduce income taxes due dollar-for-dollar, but only until income taxes due equal $0. For example, if income tax owed is $300, and the taxpayer has a non-refundable credit of $1,000, the non-refundable credit is only worth $300. The remaining $700 credit is lost.

Refundable credits also reduce income taxes due dollar-for-dollar, but they are not limited. Once refundable credits have reduced income taxes due to $0, the remainder of the credit is used to reduce other taxes (for example, self-employment taxes) or to increase a refund.

The child tax credit can be used for dependent children who have not yet turned 17 years old at the end of the tax year. This credit has both a non-refundable and a refundable portion. It has been increased to $2,000 per dependent child, with $1,400 of that amount as a refundable credit.

The dependent tax credit is a new credit that can be used for dependents who are older than 16 years old at the end of the year, and other specified relatives. This non-refundable credit is worth $500 per dependent.

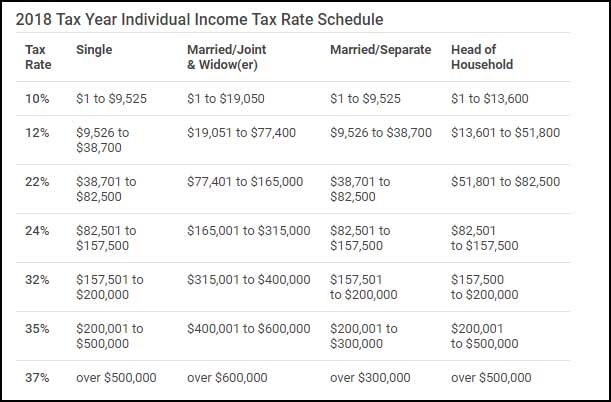

Tax brackets

Tax brackets are applied to “taxable income,” not “total income.” Brackets are progressive, rather than flat. This means that different tax rates apply to taxable income as it is “stacked” to get to a taxpayer’s final “marginal tax bracket.”

Tax penalties

For taxpayers without health insurance, the individual shared responsibility payment has changed. Starting Jan. 1, 2019, taxpayers without health insurance will no longer pay a penalty.

For taxpayers with children in school, distributions from 529 tuition plans can now be used for tuition and fees for private primary and secondary schools. The maximum tax-free distribution from these plans is limited to $10,000 per beneficiary per year.

Church tax issue

The biggest change for church congregations and other nonprofits is the new Nonprofit Parking Tax, which became effective Jan. 1, 2018. The IRS issued a “safe harbor” method in December 2018: (1) Nonprofit employers must allocate a portion of total parking expenses to reserved employee parking. (2) If more than 50 percent of the rest of the parking facility is used by the general public, then no expenses related to the unreserved parking spaces are subject to the tax.

Basically, this means that if a church or other nonprofit does not have reserved spaces for employee parking, it will not be subject to the nonprofit parking tax.

Deb Oskin, EA, NTPI Fellow, is a member of Living Peace Church of the Brethren, Columbus, Ohio. She operates an independent tax service specializing in clergy taxes and leads the annual Clergy Tax Seminar offered by the Brethren Academy for Ministerial Leadership.